Now I am no financial advisor, my opinions on this count for nothing, I wouldn’t like to think anybody takes what I say seriously, I am just thinking out loud and sharing my findings. I’m just a guy bumbling through life who spends little and saves a lot and experiences returns. I’m happy to share and talk about experiences of investments I get into, I do make bad ones and I do make good ones, but each person must make their own minds up.

Somebody recently sent me a link to www.propertypartner.co to ask me my thoughts on it as an investment.

First of all the obvious benefit is that you’re getting a property investment without the mortgage, but also without the roof over your head. You still need somewhere to rent. If you find yourself renting and your rent is a couple of quid less than what the mortgage would be, then here’s a chance to make a couple of % the difference.

I asked around and quickly found a friend who had been using this service. He told me the following:

I’d say I am getting 5% returns at a rough reasonable guess. What I like is that you get rental income and benefits of any house price rises combined. So I now have my foot on the property ladder in London. Nothing beats stocks and shares but I just find it kind of fun to be able to diversify in all the major investment groups with very little capital and also the quick and painless exit procedures help.

5% is what I see as the minimum requirement to grow savings and beat inflation. It’s not going to make you rich but it should, if you save aggressively enough, keep you out of the poor house.

Do the maths. At 5%, if you start at 20 and do just £100 a month, you should end up with £200k at 65, which would return you about £10k a year from then on. (You really have to start early lads, please listen to me, you really mus not underestimate the benefits of saving early on, even a little in your late teens and early 20s makes a huge, huge difference to you quality of life in your 30s.

That’s OK, this 5%. It’s better than leaving it in the bank, it’s much better than spending it in a nightclub or on Armani Jeans or something stupid. At 30 you would have £15,000 in the bank. It’s OK, it’s a start. I’d prefer to try and do £200 a month and make it £30,000 if possible.

Now the tax situation needs considering. The 5% is a lower return than I get in stocks and all my stock gains are protected in an ISA which makes an enormous difference. My stocks in an ISA are protected from taxation theft.

This is what I need to know about taxes if I choose to invest in Property Partner.

Your investment in property on the platform is made via the purchase of shares in basically a company, established specifically for purchasing that individual property.

Company Level Taxation

The profit made by that company is subject to corporation tax at 20%, which the company will pay directly to HMRC. In addition should the property price increase, corporation tax is payable on the gain upon disposal.

Neither of these things I need to worry about, outside of the fact they eat some of my profits before I get them. My friend is, however, estimating he is getting 5% AFTER these costs. It’s just important I understand how the investment vehicle works.

Personal Level Taxation

So what about my personal taxes which will subsequently come directly out of these 5% gains?

I should seek independent tax advice; but here’s how I think it affects me.

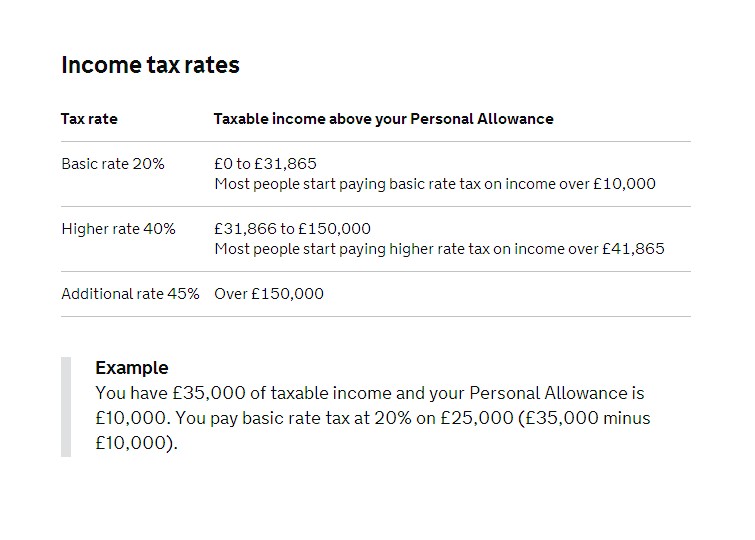

Dividends Received from Property Partner are subject to personal taxation. However, HMRC provide a 10% tax credit against dividends to compensate for tax already paid at the company level. As a result, basic rate taxpayers will be liable for no additional tax on this income. However, higher rate taxpayers will be subject to 25% tax and additional rate taxpayers will be subject to 30.6% tax.

This being the case, it could be a decent investment vehicle for kids in their teens and 20s, since they will likely be able to benefit from the tax break and thus have less requirement for the ISA protection on this investment.

There are more taxes though. There is the capital gains tax when you sell. If you sell the investment at a profit, you may have to pay capital gains tax.

UK taxpayers receive an annual tax-free allowance on capital gains tax of £11,000. Annual capital gains below £11,000 will not be subject to capital gains tax. If you’ve made more capital gains than this in the tax year, the gains will be taxable at 18% for basic rate taxpayers and 28% for higher or additional rate taxpayers.

This means, I think, that I will be safe to receive my 5% gains as long as my income, including these gains, don’t push my annual income into the higher tax bracket. When I come to sell my investment, anything I make over £11k will have 18% deducted, assuming I am still at that time in the lower tax bracket.

Confusing? Maybe, maybe not. I am not convinced on this as an investment vehicle. I need to talk to my accountant and just take it for a spin. I’ve decided to chuck some money in, I’ll start with £1000 and just leave it for year. I’ll then come back next year and let you all know what the profit was and what the costs were, plus what my accountant told me and you will then have some kind of measurement to consider in your evaluations, if this were something you were considering.